Transformations

A Transform is a composable, callable mapping Expr -> Expr.

Bijective transforms additionally implement inverse and

log_det_jacobian, so they can double as a distribution bijector via

TransformedDistribution.

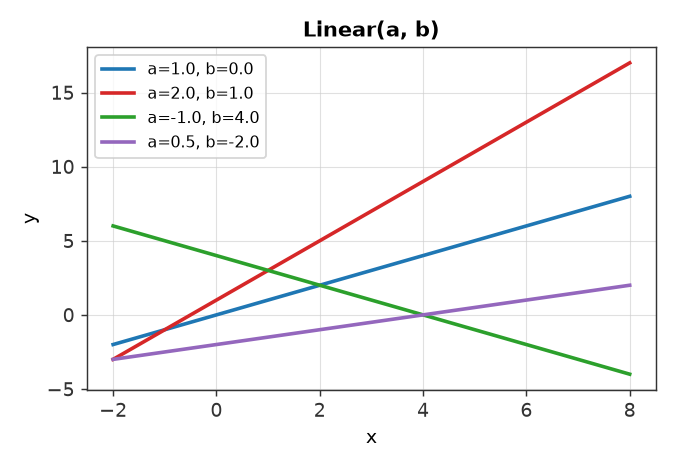

a * x + b — bijective, with closed-form inverse.

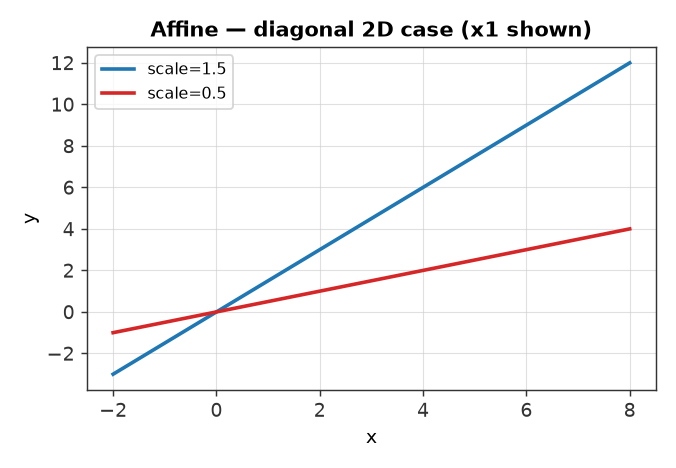

A @ x + b for vector-valued x.

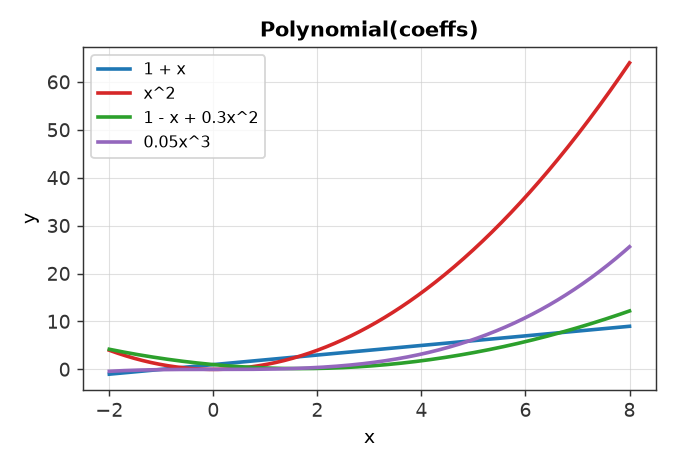

sum_i coeffs[i] * x**i.

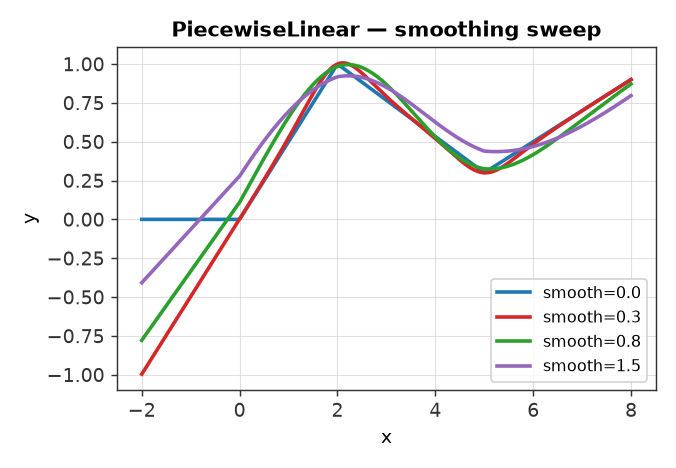

smooth=0 gives the exact (subgradient) curve; smooth=tau

blends neighbouring segments for a fully continuous gradient at the

knots.

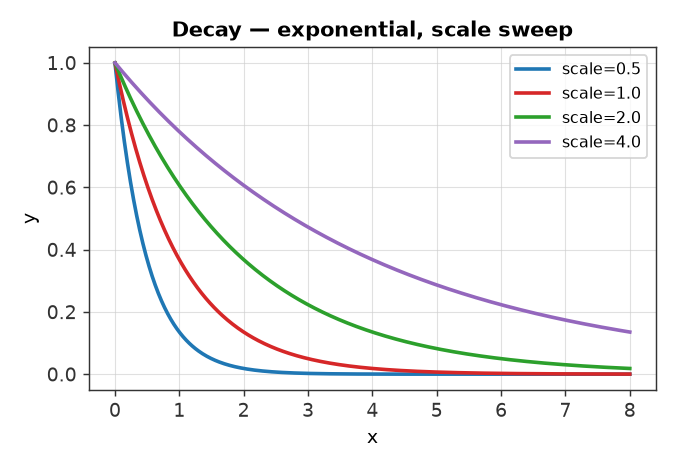

Exponential (exp(-x/scale)) or power-law decay, typically

composed after a distance primitive.

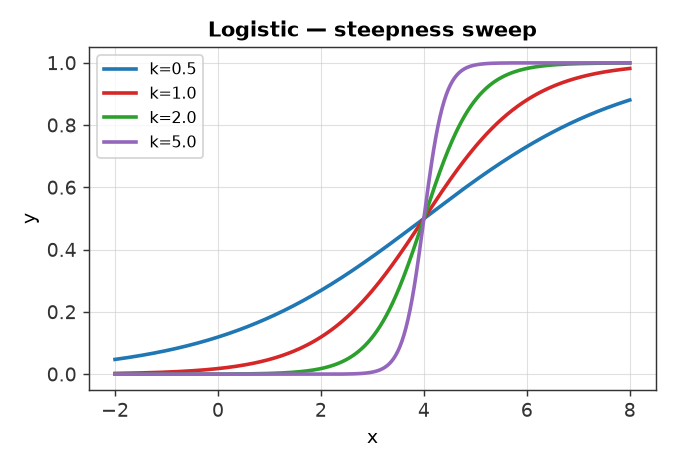

Dose-response / regulatory-acceptance curves.

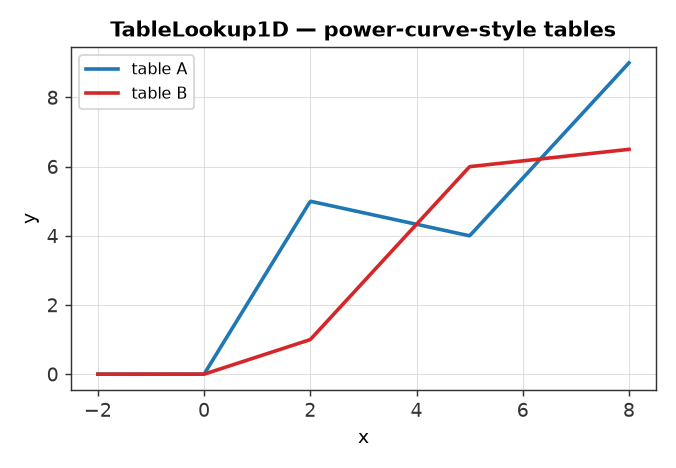

Interpolated 1D characteristic curve (e.g. a power curve).

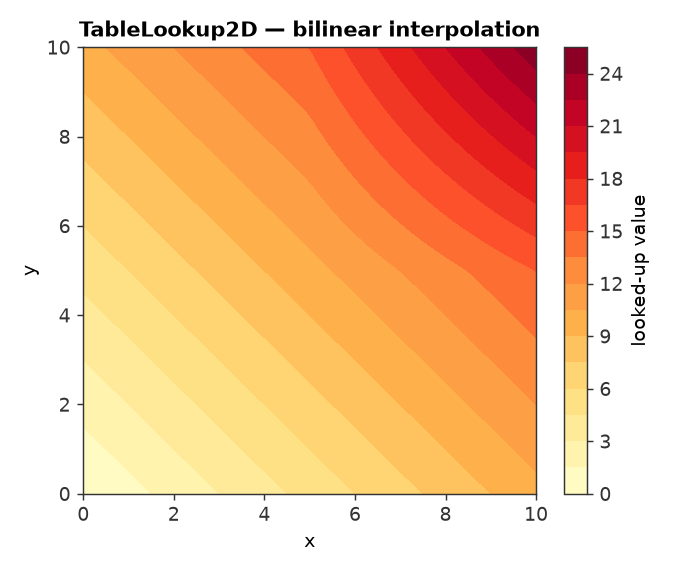

Bilinearly interpolated 2D lookup (e.g. sound power level over wind speed x direction).

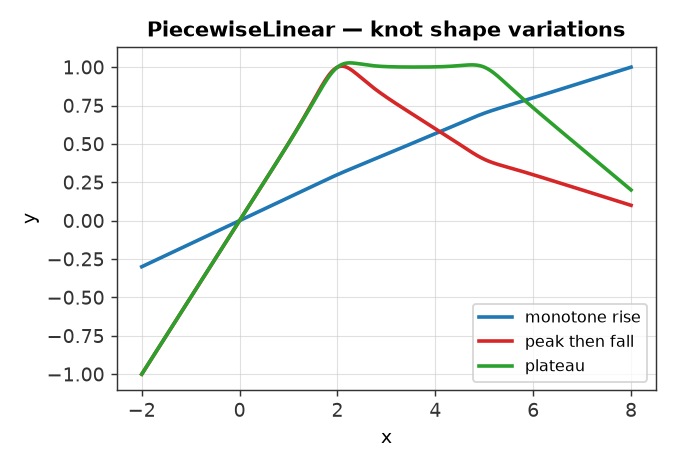

Smoothing behavior of PiecewiseLinear

Because a hard piecewise-linear kink has a discontinuous gradient at each

knot, PiecewiseLinear lets the smoothing temperature trade exactness

against gradient continuity:

A smooth value that is too large relative to the knot spacing will

blend in neighbouring segments’ slopes even at points deep inside one

segment — worth checking for if a transformed probability unexpectedly

drifts outside its valid range (e.g. below 0 for a probability fed into

Bernoulli).

- class prophys.transformations.Transform[source]

Base class for symbolic transformations.

Subclasses implement __call__. Bijective transforms additionally implement inverse and log_det_jacobian so they can be used to build a TransformedDistribution.

- class prophys.transformations.Linear(a=1.0, b=0.0)[source]

y = a * x + b(scalars or broadcastable arrays; a, b may be Expr, e.g. Param, making the slope/intercept learnable).- Parameters:

a (Any)

b (Any)

- class prophys.transformations.Affine(A, b=0.0)[source]

y = A @ x + bfor vector-valued x.- Parameters:

A (Any)

b (Any)

- class prophys.transformations.Polynomial(coeffs)[source]

y = sum_i coeffs[i] * x**i(coeffs may contain Expr values).- Parameters:

coeffs (Sequence[Any])

- class prophys.transformations.PiecewiseLinear(knots, values, smooth=0.0)[source]

A piecewise-linear curve through

(knots[i], values[i]), clamped flat beyond the endpoints.smooth=0 (default) gives the exact, subgradient-valid PWL function (matches e.g. a dose-response table exactly). smooth=tau > 0 uses a soft segment-blend so the gradient is continuous across knots too, useful when knot locations themselves are being optimized.

- class prophys.transformations.Decay(scale=1.0, kind='exp')[source]

Exponential (

exp(-x/scale)) or power-law (x**(-p)) decay, typically composed after a distance primitive.- Parameters:

scale (Any)

kind (str)

- class prophys.transformations.Logistic(x0=0.0, k=1.0, L=1.0)[source]

Dose-response curve:

L / (1 + exp(-k * (x - x0))).- Parameters:

x0 (Any)

k (Any)

L (Any)

Periodic & recurring phenomena

For seasonal, diurnal, tidal, or otherwise recurring signals — and for the “return period” framing common in extreme-event risk (e.g. a “100-year flood”).

- class prophys.transformations.Phase(period=1.0)[source]

Wrap a continuous variable (e.g. elapsed time) into

[0, period), e.g. turning “hours since start” into “hour of day”.Uses floor-modulo, which is continuous except at the wrap points (measure zero) — the same character as the library’s other hard boundary primitives (PiecewiseLinear with

smooth=0, polygon containment).- Parameters:

period (Any)

- class prophys.transformations.Periodic(period, amplitude, phase=None, offset=0.0)[source]

A learnable finite Fourier series: the standard, fully differentiable building block for seasonal/diurnal/tidal signals.

y = offset + sum_k amplitude[k] * cos(2*pi*k*x/period - phase[k])amplitude and phase are sequences of per-harmonic coefficients (length = number of harmonics); all may be Expr (typically Param), so the shape of a seasonal cycle can be learned from data via the same fit_distribution/calibrate/finetune machinery used elsewhere.

- Parameters:

period (Any)

amplitude (Sequence[Any])

phase (Sequence[Any] | None)

offset (Any)

- class prophys.transformations.ReturnPeriod[source]

Convert an annual exceedance probability to a return period (the familiar “100-year flood” framing) and back.

return_period = 1 / exceedance_probabilityBijective and defined for

p in (0, 1]; use inverse to go from a target return period back to the probability a per-event/per-year model needs to reproduce it.

- class prophys.transformations.RecurrenceRate[source]

Convert a mean inter-event time (period) to an event rate, the natural parameter for a Poisson process modeling recurring hazards (equipment failures, extreme-weather events, …).

rate = 1 / mean_interval, composable with Periodic (a time-varying rate) to build a non-homogeneous Poisson process: sample counts over a window viaprp.Poisson(rate_transform(t_window)).